THE END OF FRAGMENTATION

Cristian, monetary companies developed for many years in vertical silos. Why is that mannequin breaking down now, notably in FX and buying and selling?

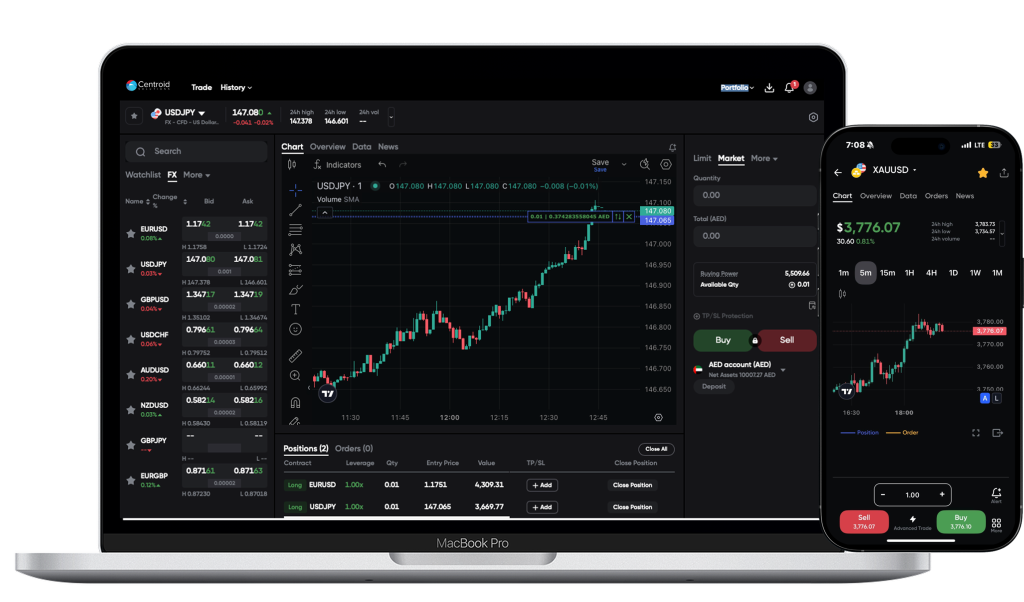

In the event you have a look at FX brokers and buying and selling establishments, fragmentation has at all times been a constraint. Buying and selling techniques, danger engines, shopper cash, funds, and reporting have been usually dealt with by separate platforms that needed to be stitched collectively.

What has modified is not only know-how, however expectation. Right now’s shoppers, whether or not retail or institutional, don’t distinguish between funding, buying and selling, transferring, or managing publicity. They anticipate a steady, real-time expertise delivered by a single interface.

In FX particularly, the place margin, liquidity, and publicity are continually shifting, siloed techniques merely can’t sustain. The business is shifting from product-centric considering to system-centric considering, the place buying and selling, funds, and account constructions function as one.

What’s necessary so as to add is that this convergence is felt most strongly on the entrance finish. Shoppers don’t see backend techniques, however they instantly really feel friction in onboarding, funding, or navigation. Fragmentation in the end reveals up as a damaged journey, and that’s the place establishments are dropping shoppers.

Now we have seen this mannequin succeed at scale with platforms like Revolut and Robinhood. Why hasn’t it develop into the norm throughout brokers and banks?

It is because what individuals see is the interface, not the infrastructure beneath. These platforms work as a result of they have been constructed on unified architectures from day one, however simply as importantly, they have been constructed with expertise possession in thoughts.

Most FX brokers and banks function on layered legacy stacks that have been by no means designed for this stage of integration or real-time management. Usually, you will notice a buying and selling platform optimized for buying and selling, a bridging engine optimized for execution, a separate pockets or fee system, one other layer for onboarding and compliance, and reporting added on prime.

Traditionally, buying and selling platforms have been additionally designed to be reused throughout many brokers with the identical entrance finish. That created scale for distributors, nevertheless it eliminated differentiation for brokers. If a shopper is sad, they’ll transfer to a different dealer utilizing the identical app, the identical interface, and the identical expertise – simply with a special brand.

That lack of differentiation creates little or no stickiness, particularly when shopper acquisition prices are excessive. Platforms like Robinhood or eToro succeeded not due to plumbing alone, however as a result of the expertise itself grew to become the product.

WHY CONVERGENCE IS HARDER THAN IT LOOKS

What are the largest structural obstacles FX brokers and banks face when making an attempt to modernize?

The largest problem is that almost all core buying and selling and banking techniques have been constructed incrementally, not architected as ecosystems. In FX, brokers are being requested so as to add new asset courses, assist extra jurisdictions, supply on the spot funding and withdrawals, present real-time danger and P&L visibility, and combine with a number of liquidity sources. Banks supporting these flows face related strain, usually performing as liquidity suppliers, custodians, or settlement companions, however on infrastructure that prioritizes stability over flexibility.

On the identical time, many establishments are nonetheless locked into platforms the place innovation on the entrance finish is constrained by backend limitations. The plumbing works, nevertheless it doesn’t help you rethink how shoppers are onboarded, engaged, or retained.

The result’s a rising hole between what the market expects and what present techniques can realistically ship with out structural change.

Is that this the place establishments usually go fallacious in digital transformation?

Sure, and it normally comes from assuming there’s a single transformation path for everybody.

Convergence is inevitable, however the way you get there is dependent upon whether or not you’re a dealer, a financial institution, or a hybrid establishment. A dealer targeted on execution and shopper expertise has very totally different priorities from a financial institution offering balance-sheet assist or Banking-as-a-Service (BaaS).

That’s precisely why we designed the One Centroid Ecosystem round a single structure that helps a number of working fashions, whereas leaving expertise design firmly within the fingers of the shopper. No two establishments needs to be pressured into the identical entrance finish or the identical journey.

From Market Actuality to Structure

For FX brokers, convergence isn’t an summary development. Buying and selling platforms more and more sit on the heart of broader monetary journeys, intersecting with funds, wallets, custody, and controlled banking rails.

The problem isn’t whether or not these elements ought to join, however how they’ll accomplish that with out compromising execution high quality, danger management, or the power to innovate on the product layer.

On the identical time, banks supporting FX move as liquidity suppliers, custodians, prime brokers, or BaaS companions face a associated problem: methods to allow innovation round trading-led ecosystems whereas preserving stability on the core.

At Centroid, this led to a foundational design precept behind the One Centroid Ecosystem: one structure, a number of working fashions, and full freedom on the entrance finish.

BANKS AS FINTECH ENABLERS: PARALLEL INFRASTRUCTURE BY DESIGN

How does this structure work in observe for banks that assist brokers and fintechs?

For banks, the strategic query isn’t methods to rebuild their complete digital stack. It’s methods to allow innovation with out destabilizing the core.

Many banks are shifting towards a fintech-enablement mannequin, offering regulated banking, custody, and settlement rails to fintechs, brokers, and client platforms by Banking-as-a-Service (BaaS). In that context, system substitute is neither sensible nor crucial.

When a financial institution acts as a fintech enabler, the target is isolation and management. You need innovation on the edge with out contaminating the core, whereas nonetheless permitting fintechs to construct differentiated shopper journeys.

How does this ‘parallel mannequin’ appear to be contained in the One Centroid Ecosystem?

Below the One Centroid Ecosystem, banks deploy a parallel, trendy infrastructure layer particularly for fintech packages.

A brand new core banking occasion, devoted to fintech exercise, runs alongside the financial institution’s present core. It communicates with legacy techniques the place required, consumes and distributes companies by way of true BaaS, and operates independently from retail and company banking.

This ensures fintech progress doesn’t introduce operational or regulatory danger into core banking operations, whereas nonetheless permitting fintechs and brokers to innovate freely on the software layer.

The place does shopper onboarding and compliance sit inside this mannequin?

On the heart sits CS Maystro, our multi-tenant Consumer Lifecycle Administration platform. CS Maystro handles digital onboarding, KYC/AML, and compliance workflows, integrates fee suppliers and multi-currency pockets companies, and helps limitless fintechs in remoted tenants.

What’s essential is that every fintech or dealer can outline its personal onboarding logic and buyer journey, whereas the financial institution retains centralized oversight and reporting. Compliance turns into a shared framework, not a constraint on expertise.

How are buying and selling, execution, and danger dealt with?

Every fintech or dealer receives a devoted occasion of Centroid’s C2C buying and selling platform backend, giving them full management over merchandise, asset courses, and payment constructions.

Execution and danger are centralized by CS 360, our unified OMS and liquidity engine. This permits establishments to scale fintech exercise whereas preserving income seize, compliance, and management – with out forcing everybody into the identical entrance finish or consumer expertise.

BROKERS, SUPER-APPS, AND DIGITAL-FIRST PLAYERS: THE ECOSYSTEM IS THE PLATFORM

How does this differ for FX brokers, neo-brokers, and super-apps working their very own shopper expertise?

The truth could be very totally different. Brokers and digital-first platforms are instantly chargeable for the end-to-end shopper expertise. For them, convergence can’t be bolted on. Working fragmented techniques with a generic entrance finish creates churn. Shoppers examine experiences, not simply spreads or product lists. That’s the reason these establishments want unified onboarding, funding, buying and selling, and account constructions, seamless fund mobility, constant compliance, real-time visibility, and a single knowledge layer.

Simply as importantly, they want the power to construct their very own entrance ends, publish apps beneath their very own model, and repeatedly evolve the expertise. Constructing entrance ends in the present day isn’t prohibitively costly. What issues is having an API stack that doesn’t restrict creativity.

Centroid’s C2C platform was constructed with this in thoughts, providing a complete API layer for shoppers who need to construct from scratch, in addition to white-labeled entrance ends for many who need pace to market.

EXPERIENCE AS THE SOURCE OF STICKINESS

The place is actual aggressive differentiation shifting in in the present day’s buying and selling and fintech platforms?

What we see throughout the business is that backend plumbing, whereas important, is not the place worth is created. It has develop into a commodity.

The actual differentiation – and the true stickiness – comes from how establishments design their shopper journeys, how they maintain customers inside their app, and the way they flip infrastructure into engagement.

Brokers make investments closely in shopper acquisition. If the expertise is generic, these shoppers are misplaced shortly to rivals utilizing the identical platforms. If the expertise is differentiated, intuitive, and repeatedly evolving, the app turns into the shopper’s monetary house.

That’s the transformation Centroid is enabling.

![Best Hyperliquid Referral Code in 2026: [HYPERLIQUIDREVIEW]](https://i0.wp.com/www.cryptoninjas.net/wp-content/uploads/hyperliquid-referral-code.jpg?w=75&resize=75,75&ssl=1 "Best Hyperliquid Referral Code in 2026: [HYPERLIQUIDREVIEW]")

{kind=link}