Analyst Weekly, February 16, 2026

Software program simply had its worst non-recession droop in 30 years. Over the previous 12 months, the group has fallen greater than 30% at its worst level which is the deepest drawdown exterior of a recession in three many years. Roughly $2 trillion in market worth has been erased, and Software program’s weight within the S&P 500 has dropped from 12% to eight.4%.

What spooked the market?

Two forces hit directly:

AI anxiousness. Buyers started pricing in a situation the place new massive language fashions would cannibalize conventional software program sooner than incumbents might adapt.

Technical capitulation. De-risking accelerated. Brief curiosity in large-cap software program moved towards cycle highs. Sentiment turned decisively bearish. Promoting turned broad: high quality names and speculative progress alike had been hit.

The market successfully priced in a “worst-case AI disruption” narrative.

However, fundamentals didn’t collapse

Consensus expectations for 2026 nonetheless name for:

~16% gross sales progress; ~17% earnings progress

Slight margin growth

Current earnings assist that resilience:

Each S&P 500 Software program firm reporting to this point beat earnings.

Income beats are operating above latest averages.

Progress stays strong double-digit.

In the meantime, valuations have compressed materially:

Ahead P/S multiples have fallen by roughly 4 turns.

Ahead P/E has dropped by greater than 10 factors.

Present multiples sit close to ranges seen throughout prior market stress episodes.

In different phrases, costs have reset sooner than fundamentals.

Supply: Bloomberg. Knowledge as of February 15, 2026.

AI: menace or tailwind?

In our view, the near-term actuality is extra nuanced than the headlines.

Enterprise software program is embedded in multi-year contracts with excessive switching prices. AI instruments are more and more being layered into workflows reasonably than changing them outright. In lots of circumstances, AI seems to be additive, creating cross-sell and upsell alternatives, and never instantly disruptive.

Long run, the construction of the business might evolve. However over the following 3 to six months, the market might have discounted a disruption curve that’s too aggressive.

Why this issues for buyers

For buyers, this setup creates two angles:

Tactical rebound potential: Excessive pessimism & brief positioning & earnings season suggest a fertile floor for sharp reversals if outcomes or steerage problem the bearish narrative.

We’re watching upcoming catalysts:

A busy calendar of software program earnings within the coming weeks.

Investor days the place administration groups can immediately deal with AI issues.

If positioning resets, rebounds will be swift, particularly in higher-quality segments like cybersecurity and mission-critical enterprise platforms.

Longer-term high quality publicity at decrease entry factors: Many large-cap software program corporations nonetheless generate robust free money stream, keep sturdy buyer bases, and are rising buybacks. In actual fact, buyback execution in software program has grown meaningfully over the previous two years, which might present further assist at depressed valuations.

Some corporations are seen to be comparatively extra insulated as a consequence of their positioning inside enterprise methods, safety infrastructure, or vertical niches. Right here’s how that panorama breaks down.

Enterprise & Mission-Essential Platforms

These platforms sit on the middle of enterprise structure. Their merchandise are sometimes tied to multi-year contracts, mission-critical workflows, and excessive switching prices; components that may reasonable near-term displacement threat. Right here, we’ve got corporations reminiscent of:

Microsoft (MSFT): Azure continues to scale as a foundational cloud and AI infrastructure layer.

ServiceNow (NOW): Workflow automation platform embedded throughout massive enterprises.

Oracle (ORCL): Database and cloud infrastructure spine with AI capabilities layered in.

SAP: Core ERP methods deeply built-in into international company operations.

Cybersecurity

Safety spending is often seen as important reasonably than discretionary. AI instruments are more and more being included into menace detection and response, suggesting integration reasonably than substitute within the close to time period. Right here, we’ve got corporations reminiscent of Palo Alto Networks (PANW);CrowdStrike (CRWD); Zscaler (ZS); Okta (OKTA); SentinelOne (S).

Knowledge & Infrastructure

As AI adoption expands, demand for knowledge storage, processing, monitoring, and safe connectivity stays central to enterprise operations. Infrastructure layers typically scale alongside application-level innovation. Right here, we’ve got corporations reminiscent of Snowflake (SNOW); Datadog (DDOG); Twilio (TWLO); Verify Level (CHKP)

Utility & Vertical Software program

Vertical software program suppliers typically function in specialised industries with regulatory complexity and customised workflows. Lengthy contract durations and domain-specific integration can contribute to income visibility. Right here, we’ve got corporations reminiscent of:

Tyler Applied sciences (TYL): Public sector software program supplier.

Guidewire (GWRE): Insurance coverage core methods.

SailPoint (SAIL):Id governance options.

JFrog (FROG): DevOps and software program provide chain tooling.

Q2 Holdings (QTWO): Digital banking software program.

CoStar (CSGP): Actual property knowledge and analytics platform.

Throughout all these classes, the frequent thread is structural embeddedness: methods that enterprises depend on each day. Whereas AI is reshaping software program broadly, the diploma and pace of disruption might fluctuate considerably relying on how central a platform is to operational infrastructure.

Funding Takeaway: The market is pricing in extreme AI disruption. The info, to this point, exhibits resilient progress and earnings beats. Additional draw back can’t be dominated out as volatility stays elevated. However in our view, the danger/reward profile has shifted. When sentiment is that this damaging and fundamentals stay intact, the steadiness of dangers typically begins to favor restoration reasonably than continued collapse. For retail buyers, the important thing query just isn’t whether or not AI adjustments software program: it can, however not uniformly. The query is whether or not at present’s costs already assume an excessive amount of harm, too quickly.

Large in Japan: The Comeback Commerce No person’s Crowded Into

For years, Japan was the market equal of “seen at 9:41pm.” Buyers glanced… then went again to the S&P 500.

However 2026? Completely different vibe.

Begin with valuations. Whereas US shares commerce north of 20x earnings, Japan’s sitting nearer to the mid-teens. Not distressed. Not bubbly. Simply… cheaper. And earnings are literally enhancing.

Then there’s reform vitality. The Tokyo Inventory Trade has been nudging corporations buying and selling under guide worth to form up: increase returns, enhance governance, unlock worth. In different phrases, company Japan is being pushed to behave extra shareholder-friendly.

Coverage’s shifting too. Japan is lastly exiting ultra-easy cash mode. Which means larger yields and a firmer yen; which sounds dramatic, however actually indicators one thing more healthy: normalization. After many years of deflation fears, Japan is reflating.

Lastly, positioning. Home buyers are nonetheless underweight equities. Add in international provide chains diversifying away from China, and Japan all of the sudden seems to be strategically related once more.

So no, we don’t assume it is a late-cycle melt-up story.

It’s a reform, reflation, and cheap valuation story.

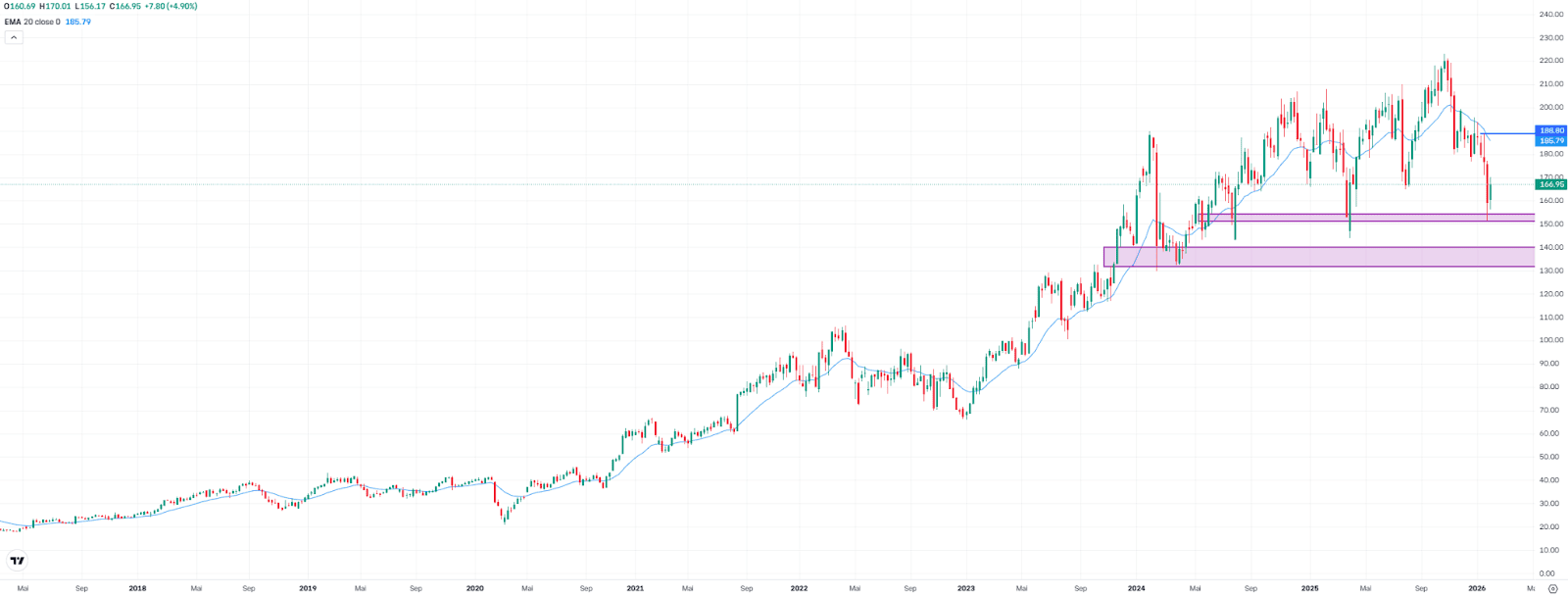

Palo Alto Networks Defends Assist – Earnings in Focus

Palo Alto Networks shares recovered 4.9% final week to $166.95. The technical set off was the profitable protection of the assist zone (Truthful Worth Hole) between $151.20 and $154.40 within the prior week. This space has already acted as a assist zone twice over the previous two years.

The rebound diminished the gap to the report excessive to round 25%, after the drawdown had briefly widened to 32%.

Quarterly earnings are due after the shut on Tuesday. They’re prone to decide whether or not the restoration continues or whether or not the long-term assist zone will face one other check.

To sustainably enhance the chart image, a transfer above the interim excessive at $188.80 can be required – that is the place the latest promoting wave started. The 20-week transferring common, presently close to $186, can be situated on this space. A break again above this degree might appeal to further consumers, however each resistance ranges would have to be cleared decisively.

On the draw back, the following related assist zone lies between $133.80 and $140.10.

Palo Alto Networks, weekly chart. Supply: eToro

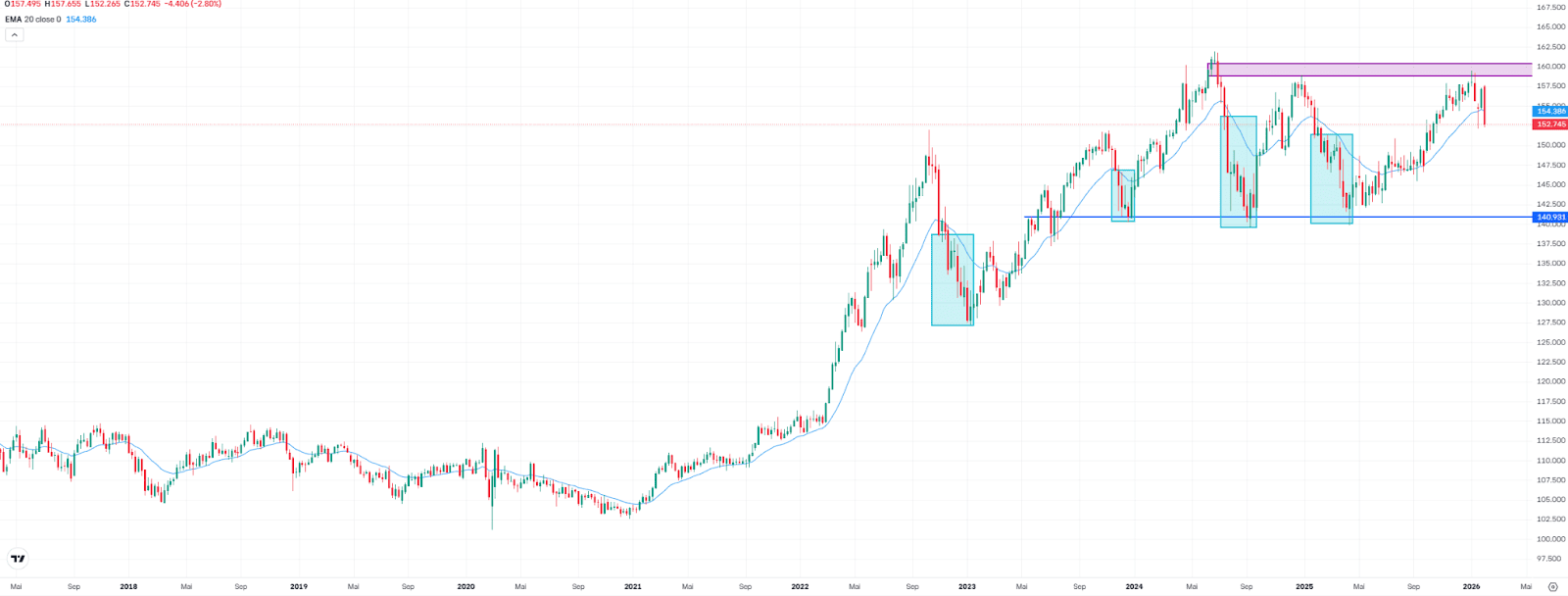

USDJPY Posts Strongest Weekly Decline Since November 2024

USDJPY fell 2.8% final week to 152.75, marking its strongest weekly decline since November 2024. Again in January, consumers had already failed at a long-term resistance zone, a Truthful Worth Hole between 158.85 and 160.33. An identical sample occurred in early 2024.

Final week, the pair not solely reversed decrease but in addition dropped under the 20-week transferring common, presently at 154.39. This indicators a short-term shift in path and will increase the probability of additional declines (see blue rectangles within the chart).

From a broader perspective, the world round 141 comes into focus as a possible draw back goal. Since 2023, this zone has been examined a number of occasions and repeatedly acted as assist.

Nonetheless, if the pair climbs again above the 20-week transferring common, one other check of the resistance zone between 158.85 and 160.33 can be doable. For now, the technical setup factors to continued promoting stress.

USDJPY, weekly chart. Supply: eToro

BTC in a Delicate Adjustment Part

Bitcoin enters a brand new week in a fragile section. The correction from the October highs is round 50%, and though we’ve got seen technical rebounds from the $60,000–62,000 USD space, structural knowledge nonetheless don’t present clear indicators of a definitive backside.

Probably the most placing transfer occurred on February 5, when the market recorded roughly $5.4 billion in realized losses in a single day. It was the biggest loss realization occasion since March 2023. At first look, it could possibly be interpreted as capitulation. Nonetheless, when the lens is widened, the context adjustments.

Cumulative losses measured in BTC phrases are round 0.3 million. Throughout the 2022 bear market, that determine exceeded 1.1 million BTC. In different phrases, the adjustment has been important, but it surely nonetheless doesn’t attain structural cleaning ranges corresponding to earlier cycle bottoms.

Basic cycle metrics reinforce that studying. MVRV has not entered excessive undervaluation territory. NUPL doesn’t replicate unrealized loss ranges typical of deep capitulation. Roughly 55% of whole provide stays in revenue, whereas at historic lows that share approached 45–50%. As well as, worth continues to commerce above the realized worth (the typical buy worth of all BTC holders), situated round $55,000 — a degree that in earlier cycles was clearly breached earlier than a base was fashioned.

Market bottoms are hardly ever remoted one-day occasions. They’re processes that require time, volatility compression, and emotional exhaustion.

On the identical time, the macro setting stays decisive. Expectations of upper charges for longer proceed to restrict threat urge for food. Till there are clear indicators of financial easing, it’s troublesome for flows to return with sustained energy to the property most delicate to liquidity, reminiscent of bitcoin.

On the institutional entrance, ETFs have recorded weekly outflows of roughly $360 million. It’s not a disorderly determine nor corresponding to systemic panic episodes, but it surely confirms that structural shopping for flows haven’t but returned decisively. Nor are we seeing huge liquidations from long-term buyers, suggesting the market is in an adjustment section reasonably than a collapse. All of this paints a transparent image: the market has corrected sharply, cleaned a part of the surplus, however nonetheless doesn’t show the basic signs of a mature backside.

This doesn’t essentially suggest that one other abrupt decline should happen. It means the method might prolong over time. Consolidation phases following main bull cycles are usually extended and require gradual rebuilding of confidence and flows.

For the investor, the message is extra strategic than tactical. It’s not about anticipating the precise backside, however about understanding the context. Within the absence of clear structural capitulation indicators and with a still-restrictive macro setting, prudence stays coherent within the brief time period.

On the identical time, the correction has already considerably diminished valuations from the highs, which begins to open home windows for gradual accumulation on longer horizons, offered one assumes volatility will stay current.

The week forward will probably not outline the cycle. However it could present clues in regards to the pace of the adjustment and the resilience of assist across the $60,000 space. In markets like this, self-discipline and endurance are sometimes extra worthwhile than the push to anticipate the flip.

This communication is for data and training functions solely and shouldn’t be taken as funding recommendation, a private suggestion, or a suggestion of, or solicitation to purchase or promote, any monetary devices. This materials has been ready with out making an allowance for any explicit recipient’s funding aims or monetary scenario and has not been ready in accordance with the authorized and regulatory necessities to advertise impartial analysis. Any references to previous or future efficiency of a monetary instrument, index or a packaged funding product are usually not, and shouldn’t be taken as, a dependable indicator of future outcomes. eToro makes no illustration and assumes no legal responsibility as to the accuracy or completeness of the content material of this publication.

Price Prediction 2026, 2027-2030")

{kind=link}