Analyst Weekly, April 7, 2026

Banks are nonetheless high quality. The straightforward positive factors will not be.

An investor doesn’t simply have a look at banks as financial institution shares. They have a look at them as a dwell learn on progress, funding, credit score and threat urge for food. Proper now, the message from banks within the US and Europe is pretty balanced: the cycle nonetheless appears to be like wholesome sufficient to help income, however the simple upside is gone.

US banks are nonetheless incomes about 11% ROE, whereas European banks are nearer to 13.4%. Valuations will not be stretched both: US banks commerce round 1.2x ahead e book and 11.9x ahead earnings, whereas European banks commerce round 1.3x ahead e book and 9.8x ahead earnings.

To us, this appears to be like like a slower-growth, but still-profitable setting.

Oil shock: from inflation story to progress story

That steadiness issues much more in an oil shock. Increased oil costs will help hold rates of interest elevated, which helps financial institution profitability within the brief time period. However the identical oil spike additionally squeezes households, cools mortgage demand, and will increase credit score threat.

If oil stays excessive, the larger hit is extra more likely to come by way of slower progress and weaker sentiment, not simply inflation.

Banks are already getting ready for that shift. Provisions (the cash put aside for potential mortgage losses) are beginning to rise despite the fact that defaults haven’t but moved considerably. That may be a forward-looking sign: banks are getting ready for softer situations forward.

Margins are peaking, funding is tightening

A extra essential shift is occurring beneath the floor. Web curiosity margins, at present round 2.9% within the US (and a couple of.4% in Europe), are possible near their peak.

Mortgage progress continues to be holding up, however deposit progress is lagging, which means banks are beginning to pay extra for funding. That sometimes marks the transition from margin growth to margin normalization.

On the similar time, valuations nonetheless indicate upside. Many giant banks, together with Barclays, Deutsche Financial institution, and UBS, nonetheless carry 20% to 50% upside to cost targets, suggesting that expectations should still be too optimistic if progress slows

The US appears to be like steadier, Europe extra delicate

The regional comparability is much less about profitability and extra about sensitivity.

European banks are delivering larger returns, however with extra publicity to macro swings, significantly power and progress. US banks, with decrease loan-to-deposit ratios (~72% vs ~88% in Europe), supply a extra secure funding base.

Funding takeaway: Banks are nonetheless making good cash, however the tailwind from larger charges is fading. Europe presents extra working leverage if progress stabilises, whereas the US presents a cleaner balance-sheet story if the macro turns into extra risky.

Regional banks deserve their very own bucket

Regional banks needs to be handled individually from giant money-center banks.

What stands out to us right here is dispersion. Regional banks are more and more buying and selling on idiosyncratic elements, resembling publicity to non-public credit score, deposit combine, or price buildings, somewhat than a single macro narrative. This marks a shift from a cycle the place banks moved collectively to 1 the place inventory choice issues extra.

Investor conversations are already specializing in:

personal credit score publicity

AI-related price pressures

potential M&A if regulation turns into extra supportive

The perfect alternatives are the place you get three issues directly:

cheap valuations

strong earnings energy

adequate capital power to soak up a softer economic system

Funding Takeaway: selective, not defensive

Banks will not be flashing pink. Capital is robust and income are wholesome. However the cycle appears to be shifting from growth to normalization. The straightforward re-rating part appears to be like behind us. The cleaner option to categorical that view is:

The chance continues to be there however it’s changing into extra selective, extra nuanced, and fewer macro-driven.

Personal Credit score: From Simple Liquidity to Late-Cycle Actuality

Personal credit score will not be the following subprime disaster. It’s, nonetheless, shifting out of an period of simple liquidity right into a extra demanding part, with indicators we’re getting into the later levels of the credit score cycle.

A part of the explanation that is unlikely to be systemic is scale. Personal credit score is a comparatively small market in comparison with the banking system, which stays properly capitalised and able to absorbing lending if wanted. Danger is not concentrated inside banks, and their direct publicity to higher-risk segments stays restricted.

That stated, stress is changing into seen. It’s rising first in additional liquidity-sensitive areas, together with retail-oriented automobiles. Portfolios additionally carry significant publicity to software program, round 20%, at a time when the sector faces uncertainty. On the borrower degree, the rising use of deferred curiosity funds suggests money movement strain is constructing.

Importantly, the preliminary strain is exhibiting up in liquidity somewhat than defaults. Some buildings supply periodic redemptions whereas holding illiquid property, and that mismatch is now being examined as buyers withdraw capital. This helps clarify why returns have appeared secure: restricted mark-to-market pricing smooths volatility, till liquidity forces adjustment.

Even so, situations stay contained. Funding is out there, secondary markets present help, and closed-end buildings restrict the chance of pressured promoting. Market pricing is reflecting this steadiness. Listed personal credit score automobiles commerce at modest reductions, and spreads, significantly in software program, have widened. However there was restricted spillover into broader credit score markets resembling high-yield bonds or leveraged loans.

The following part of threat will possible come by way of refinancing. Round 13% of personal credit score loans mature by 2026–2027, with a bigger wave additional out. If borrowing prices stay elevated, some debtors will come below strain.

Extra importantly, the main focus ought to shift from debtors to lenders. Credit score cycles not often change into systemic because of defaults alone, however when lenders are pressured to react. That shifts the main focus to establishments offering capital, together with insurers and liquidity-sensitive automobiles.

For buyers, the main focus ought to stay on high quality. Robust steadiness sheets and dependable money flows ought to outperform, whereas extra leveraged corporations are more likely to face growing strain because the cycle evolves.

Lengthy-Time period Bonds Battle for Stability

Lengthy-term bonds have come below noticeable strain in latest weeks. The iShares 20+ 12 months Treasury Bond ETF is buying and selling at $86.68 on Monday. Whereas this marks a slight restoration from the latest low of $85.44 two weeks in the past, it stays under the February excessive of $90.85, the best degree up to now in 2026.

A transparent sample has emerged over the previous yr and a half. Costs repeatedly rebound above the 2023 low of $82.30. This factors to a possible broader backside formation. On the similar time, consumers proceed to face resistance within the $92 to $94 vary. Solely a breakout above this zone would sign the top of the long-term downtrend and considerably enhance the technical outlook.

TLT. Supply: eToro

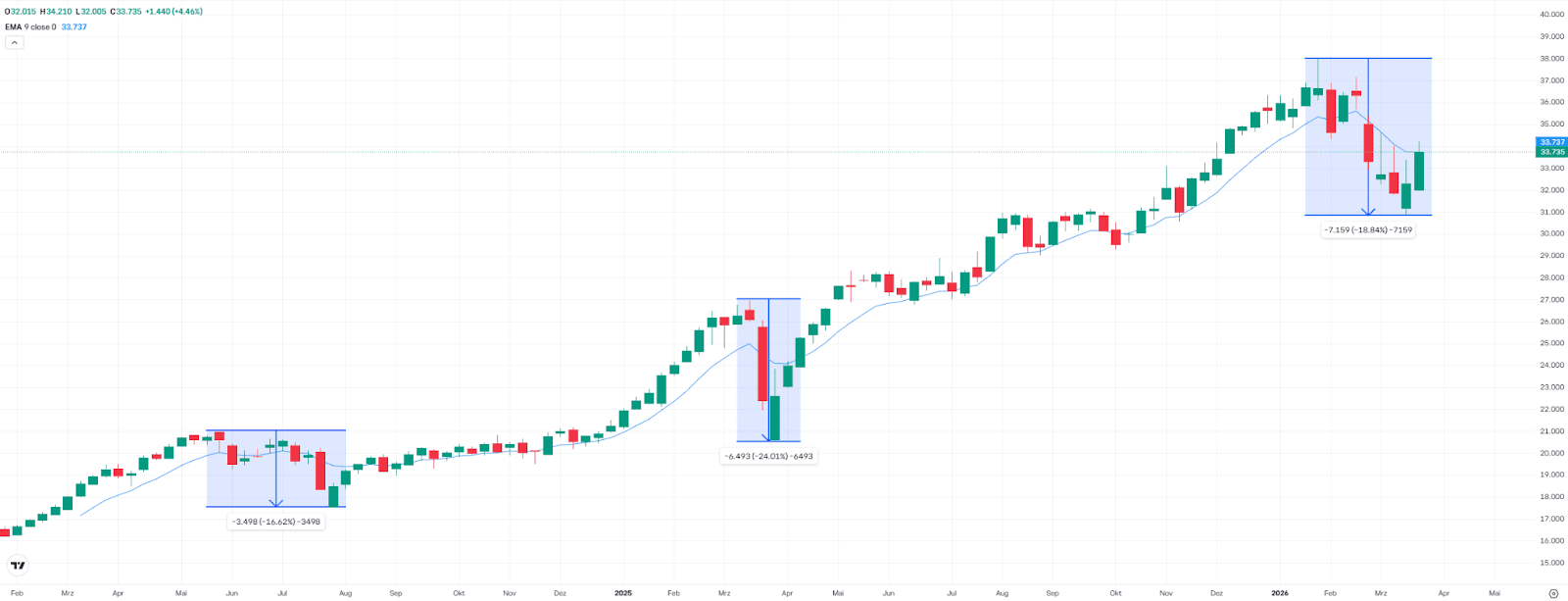

Weak spot within the Banking Sector: Traditionally a Shopping for Alternative?

The iShares STOXX Europe 600 Banks UCITS ETF is down round 4% year-to-date, buying and selling at €33.74. At one level, losses had been a lot steeper, with the ETF falling as a lot as 19% from its file excessive.

Comparable pullbacks occurred in 2024 and 2025, and in hindsight, they provided enticing entry alternatives. In phases like this, it’s essential to look at for affirmation alerts. One key indicator is a sustained transfer again above the 20-week shifting common. A wholesome uptrend is usually outlined by larger highs and better lows above this degree. For now, the market seems to be in a possible transition part.

European financial institution shares. Supply: eToro

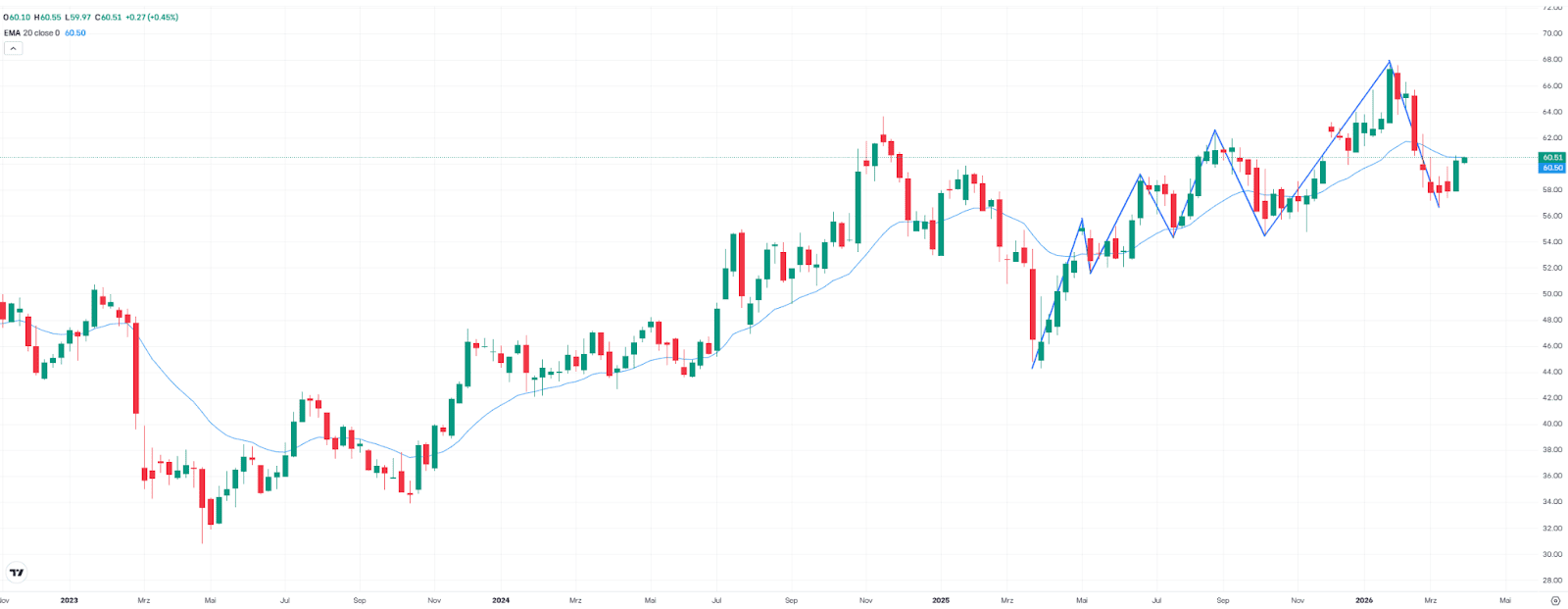

Regardless of the Promote-Off: Bulls Stay in Management of US Banks

The US banking sector was not resistant to the latest sell-off. Nonetheless, the SPDR S&P Financial institution ETF has proven relative power, already recovering its year-to-date losses. At its lowest level, the ETF was down about 16% from its February file excessive. Regardless of this pullback, the bullish construction (see Chart) that has been in place for over a yr stays intact – an indication that consumers nonetheless maintain the higher hand.

From a technical perspective, this helps the case for a continuation of the uptrend. Solely a break under the October low at $54.56 would put the development in danger. The ETF is at present buying and selling at $60.52, leaving about 10% of draw back room to this key help degree.

US financial institution shares. Supply: eToro

Bitcoin: Caught in Worth, Constructing in Construction

Bitcoin is at a well-defined technical and structural inflection level, and the hole between what value exhibits and what the underlying information says is the place the true story lives.

On the floor, the market appears to be like caught. BTC has been ranging between $65K and $75K for weeks, unable to maintain a transfer in both course. Spot volumes are down 70% from This autumn 2025 highs, and perps are off 63%. This isn’t capitulation , it’s one thing more durable to commerce: a market with out conviction, ready for a motive to maneuver.

The macro backdrop explains a lot of it. BTC continues to commerce as a high-beta threat asset, tightly correlated to an fairness market the place the Nasdaq has damaged under its 200-day shifting common. And not using a restoration in tech equities, and with charges remaining structurally elevated, the liquidity tailwind that drove the earlier cycle is just absent.

However beneath the flat value, the construction retains constructing quietly. Institutional entry is increasing, new large-scale platforms are getting ready direct BTC/ETH choices to shopper bases the place present crypto publicity sits round 5%, implying vital untapped capital. Stablecoins stand at $333bn, up $192bn in two and a half years, representing latent liquidity ready for the correct entry level. DEX market share continues to develop no matter value, and early indicators of sovereign, degree BTC positioning are starting to emerge.

That is time distribution, not value distribution. The inspiration for the following transfer is being laid in silence. The catalyst, whether or not a regulatory sign, an fairness restoration, or a shift in monetary situations, hasn’t arrived but. Till it does, the proper posture is structural conviction with out urgency. No leverage, no rush, and no mistake of complicated low volatility with low threat.

This communication is for data and schooling functions solely and shouldn’t be taken as funding recommendation, a private advice, or a proposal of, or solicitation to purchase or promote, any monetary devices. This materials has been ready with out bearing in mind any explicit recipient’s funding targets or monetary state of affairs and has not been ready in accordance with the authorized and regulatory necessities to advertise unbiased analysis. Any references to previous or future efficiency of a monetary instrument, index or a packaged funding product will not be, and shouldn’t be taken as, a dependable indicator of future outcomes. eToro makes no illustration and assumes no legal responsibility as to the accuracy or completeness of the content material of this publication.

")

{kind=link}