Analyst Weekly, September 1, 2025

Tariffs in Limbo

The US Courtroom of Appeals simply clipped US’s tariff wings. On Friday, the Federal Circuit dominated that the president can’t use emergency powers (IEEPA) to impose tariffs, saying the legislation doesn’t really give him that authority. The court docket let the tariffs keep in place till October 14 so the administration can attraction to the Supreme Courtroom. The administration will doubtless attraction to the Supreme Courtroom and search a keep, which might preserve tariffs in place till the case is set. If a keep is denied, tariffs would instantly cease being collected, successfully delivering fiscal stimulus.

Why it issues: Almost 90% of Trump’s tariffs had been enacted below IEEPA, overlaying greater than $300B in items. Whereas tariffs on autos, metal, aluminum, and copper (below Part 232) aren’t touched, this determination nonetheless strikes on the core of Trump’s commerce playbook.

Investor angle:

The true kicker isn’t whether or not tariffs stick long-term: the White Home has a Plan B to reimpose them via different channels.

The near-term drama is whether or not present tariffs will have to be refunded. If the Supreme Courtroom guidelines towards the administration, about $100B in rebates may stream again to corporations.

Layer that on high of the Fed’s price cuts, $150B in client assist, and new enterprise tax incentives and also you’ve bought a recent dose of fiscal stimulus hitting the financial system.

Firms most levered to China, Brazil, India, Switzerland, and Vietnam would see the most important aid rally if tariffs are struck down.

Tariffs presently decrease US deficits by about $4 trillion over the subsequent decade, per the CBO. If tariffs are struck down, deficits rise, which may push bond yields increased. Treasuries might dump on deficit considerations, even when equities rally on tariff aid.

Buyers shouldn’t assume tariff aid is everlasting. But when rebates are pressured via, it may hand company America an surprising windfall simply as financial and financial coverage are already easing. That cocktail would increase progress and will preserve markets buzzing.

Low Correlations Enhance Inventory-Selecting Potential However Thoughts the Imply Reversion Danger

With the S&P 500 buying and selling at file highs, rolling 90-day correlations amongst its constituents stay close to traditionally low ranges (see beneath). For traders, this normally creates an surroundings the place diversification advantages are strongest as particular person shares are much less more likely to transfer in tandem, permitting portfolios to unfold danger extra successfully.

For energetic managers, this backdrop is especially constructive. When company-specific fundamentals drive returns slightly than macro elements, inventory pickers have extra scope to generate alpha. In distinction, throughout high-correlation regimes, inventory choice tends to matter much less since “all the things strikes collectively.”

However historical past suggests this calm not often persists. Correlations are mean-reverting, and prolonged durations of low correlation, and better dispersion that comes with it, have typically been adopted by sharp spikes, usually triggered by stress occasions akin to Fed coverage shifts, geopolitical shocks, or earnings disappointments. The problem is that correlations usually are not secure: they spike rapidly in selloffs, lowering diversification advantages on the very second traders want them most.

The implication for traders is twofold. Right this moment, low correlations help diversification and reward selective positioning. However trying forward, historical past cautions towards extrapolating present circumstances into burdened markets.

Knowledge as of September 1, 2025. Supply: Bloomberg.

When Bonds Push Again: Washington’s Actual Test on Energy

The bond market is the place Washington’s financial selections get stress-tested. When Treasury yields rise, the ripple results impression key cornerstones of the financial system, specifically mortgages, bank cards, and enterprise loans all get costlier, while fairness valuations, notably in rate-sensitive sectors, come below strain. For on a regular basis traders, that makes bond market strikes simply as consequential as inventory earnings.

The latest headlines surrounding the dismissal of Fed Governor Lisa Prepare dinner are actually about testing presidential energy over the central financial institution. But, we expect the bond market holds the actual leverage. If traders lose confidence that the Fed will defend worth stability, or if fiscal deficits balloon regardless of tariffs, the bond market can punish Washington with increased yields. That transfer successfully constrains the White Home, as costlier borrowing makes fiscal growth tougher to maintain, as increased yields can derail progress by tightening monetary circumstances.

We noticed the same episode of ‘exhausting strain’ earlier than. In 2020-2021, disclosures of hawkish Fed officers’ trades led a number of governors to resign simply as inflation dangers had been constructing. That contributed to the Fed staying looser for longer, and inflation surged to its highest in a long time. Markets then pressured the Fed into aggressive tightening. The lesson is straightforward: political maneuvering can tilt coverage within the brief run, but when bond traders push again, coverage has to alter.

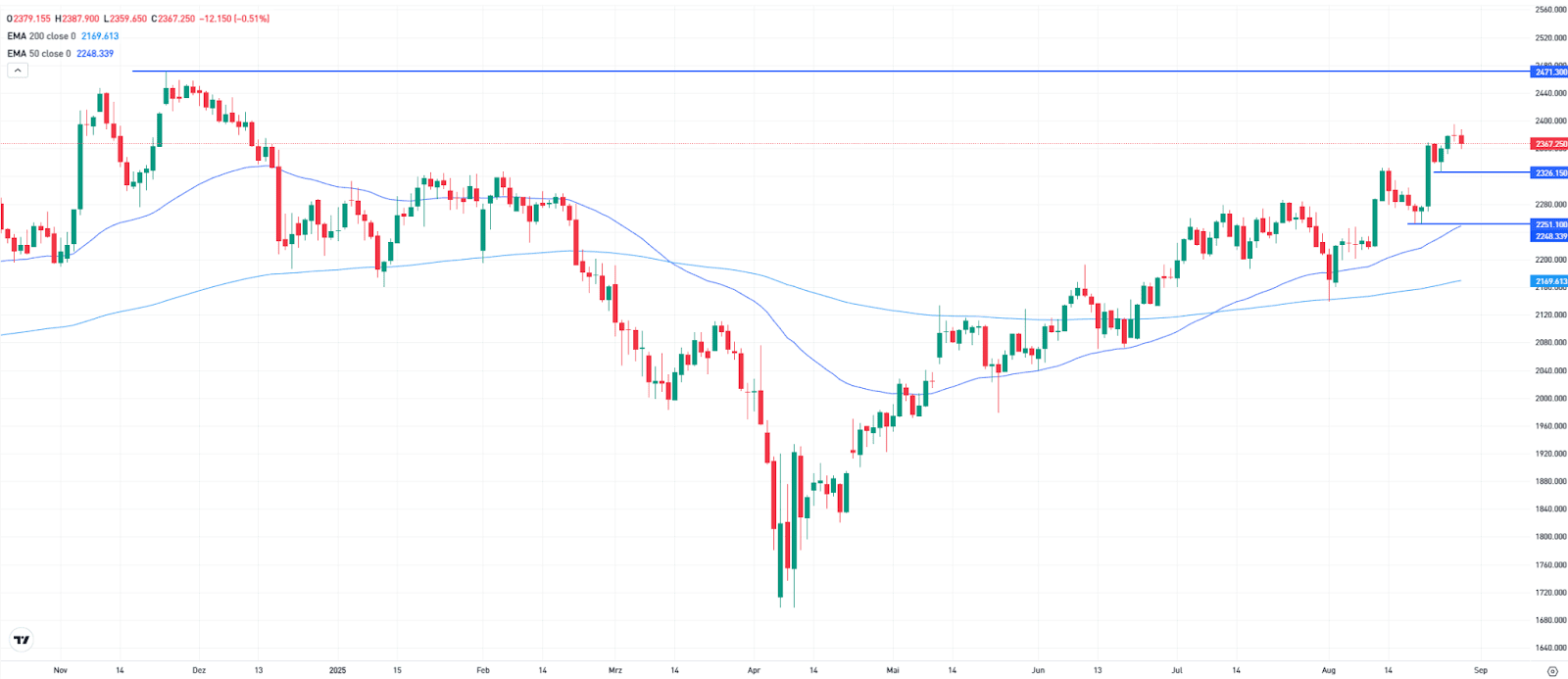

Small Caps Are Notably Fee-Delicate

Small caps have obtained little consideration in recent times however could possibly be on the verge of a comeback, particularly if the probabilities of additional price cuts enhance. Whereas the S&P 500 has gained 60.2% over the previous three years, the Russell 2000 has lagged behind with a rise of simply 25.2%. Since its April low, the index has been transferring in a secure upward development with out main setbacks and is now approaching its file excessive. That file excessive stands at 2,471 factors and is presently solely 4 to five% away. Key help ranges are at 2,326 and a pair of,251 factors, with the latter aligning with the 50-day transferring common.

Russell 2000 within the day by day chart. Supply: eToro

Weak point In The US Labor Market Doubtless To Persist

Markets are firmly anticipating a Fed price lower in September, with the chance estimated at round 86%. What stays unsure is the trail past that. Whether or not the subsequent lower is available in October or not till December continues to be unclear, it’s extra of a coin toss. The primary purpose behind the anticipated easing is the weakening labor market.

The following knowledge replace is scheduled for Friday at 2:30 p.m. In August, solely 78,000 jobs are anticipated to have been created. Weak point has already endured for a while. In July, expectations had been missed by 37,000 jobs, and figures for Might and June had been revised down by a mixed 258,000. The unemployment price is predicted to have risen from 4.2% to 4.3%.

The ISM Manufacturing PMI (knowledge due Tuesday) has been beneath the 50 mark since March. For August, a rise from 48.0 to 48.6 is forecast. The longer the index stays beneath 50 and the deeper it falls, the larger the danger of recession. The ISM Providers PMI (knowledge due Thursday) is predicted to stay above 50, with a slight enhance from 50.1 to 50.5 projected.

Buyers need to know whether or not that is merely a short lived weak point within the financial knowledge or one thing extra vital. The bigger the deviation from the anticipated values, the stronger the market response could possibly be. The labor market report is a glance within the rearview mirror, whereas the PMI knowledge function essential main indicators.

This communication is for data and training functions solely and shouldn’t be taken as funding recommendation, a private advice, or a proposal of, or solicitation to purchase or promote, any monetary devices. This materials has been ready with out bearing in mind any specific recipient’s funding targets or monetary state of affairs and has not been ready in accordance with the authorized and regulatory necessities to advertise unbiased analysis. Any references to previous or future efficiency of a monetary instrument, index or a packaged funding product usually are not, and shouldn’t be taken as, a dependable indicator of future outcomes. eToro makes no illustration and assumes no legal responsibility as to the accuracy or completeness of the content material of this publication.

Surges 27%")

{kind=link}