The Each day Breakdown takes a scoop into Chipotle, inspecting what’s going mistaken with the inventory. Is the decline sufficient to entice buyers?

Earlier than we dive in, let’s be sure to’re set to obtain The Each day Breakdown every morning. To maintain getting our day by day insights, all that you must do is log in to your eToro account.

Deep Dive

Most of us are acquainted with Chipotle, the corporate that’s well-known for its bowl and burrito choices. This fast-casual juggernaut commanded a market cap of just about $100 billion at its all-time excessive from 2024, however has struggled since, with shares down almost 40% from the height and into an fascinating technical space.

It didn’t assist that former CEO Brian Niccol — the one who helped lead an enormous turnaround on the agency — left final 12 months and went to Starbucks. From that perspective, some buyers have doubtless misplaced religion in administration’s skill to correctly steer the Chipotle ship.

The Enterprise

After we have a look at the enterprise, we will see that income, web earnings, and free money circulate have been steadily rising through the years. After we have a look at expectations for 2025, analysts anticipate income to rise 7.5% and earnings to develop 8.5%. Additional, they anticipate each figures to speed up to double-digit progress in 2026 and 2027, with earnings progress outpacing income progress (which might be good for margins).

The chance: Whereas analysts’ estimates might be spot-on correct — and even too conservative — one danger is that the estimates are too optimistic. If that’s the case, Chipotle could not develop as quick as buyers presently anticipate and that might inflict additional ache on its share worth.

One other danger? The buyer. Within the firm’s final convention name, CEO Scott Boatwright stated:

“I feel a lot of what we’re experiencing proper now is because of macro and the low-income client is searching for worth as a worth level. At current you need to look no additional than what’s happening with our rivals with snack event or $5 meals, and that’s the place the buyer is drifting in direction of, [with] worth as a worth level due to low client sentiment.”

Nevertheless, he added:

“We did see some share loss within the April-Could timeframe because the low-income client pulled again, however we’re again to share features but once more in June-July.”

Wish to obtain these insights straight to your inbox?

Enroll right here

Diving Deeper

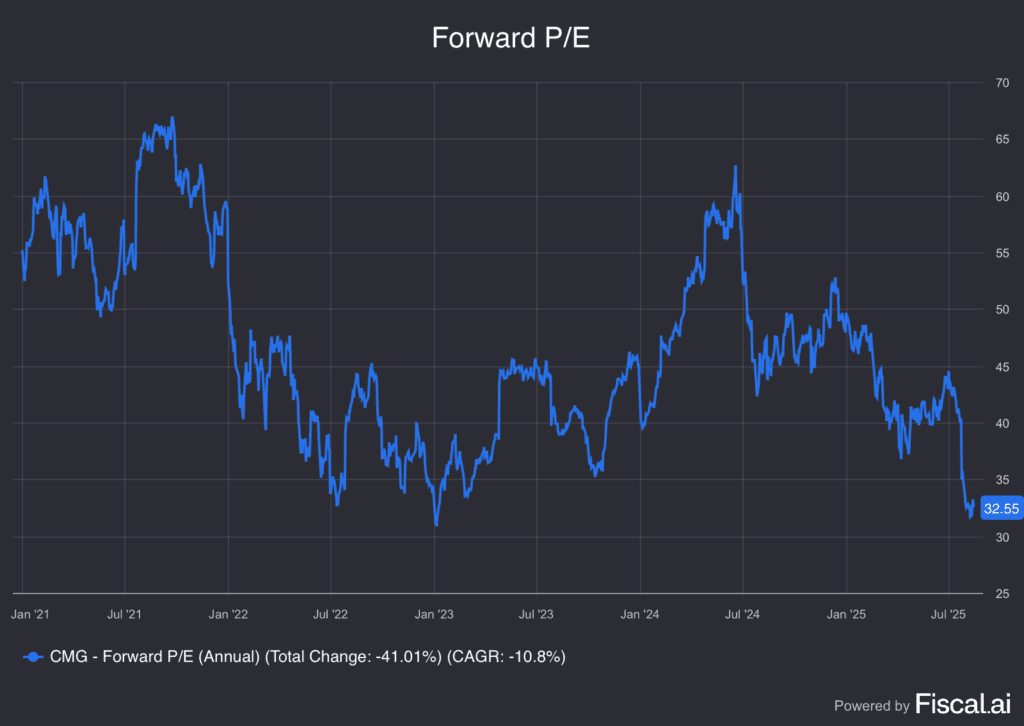

For what it’s value, analysts’ consensus worth goal requires roughly 38% upside within the inventory. With expectations nonetheless calling for progress, we’ve seen Chipotle’s valuation fall because the share worth has moved decrease.

The inventory now trades with its lowest ahead P/E ratio in additional than two years.

Bulls could determine {that a} ~40% decline within the inventory worth, strong ahead progress, and a multi-year low in its ahead valuation is sufficient to warrant a long-term place. Different buyers would possibly argue that Chipotle might be liable to an additional slowdown in its enterprise or that its valuation is just too wealthy — even when there isn’t an additional slowdown from right here.

Both means, the inventory’s decline has now introduced ahead an fascinating debate amongst buyers.

Disclaimer:

Please observe that attributable to market volatility, among the costs could have already been reached and situations performed out.

Surges 27%")

{kind=link}