Picture supply: Getty Photos

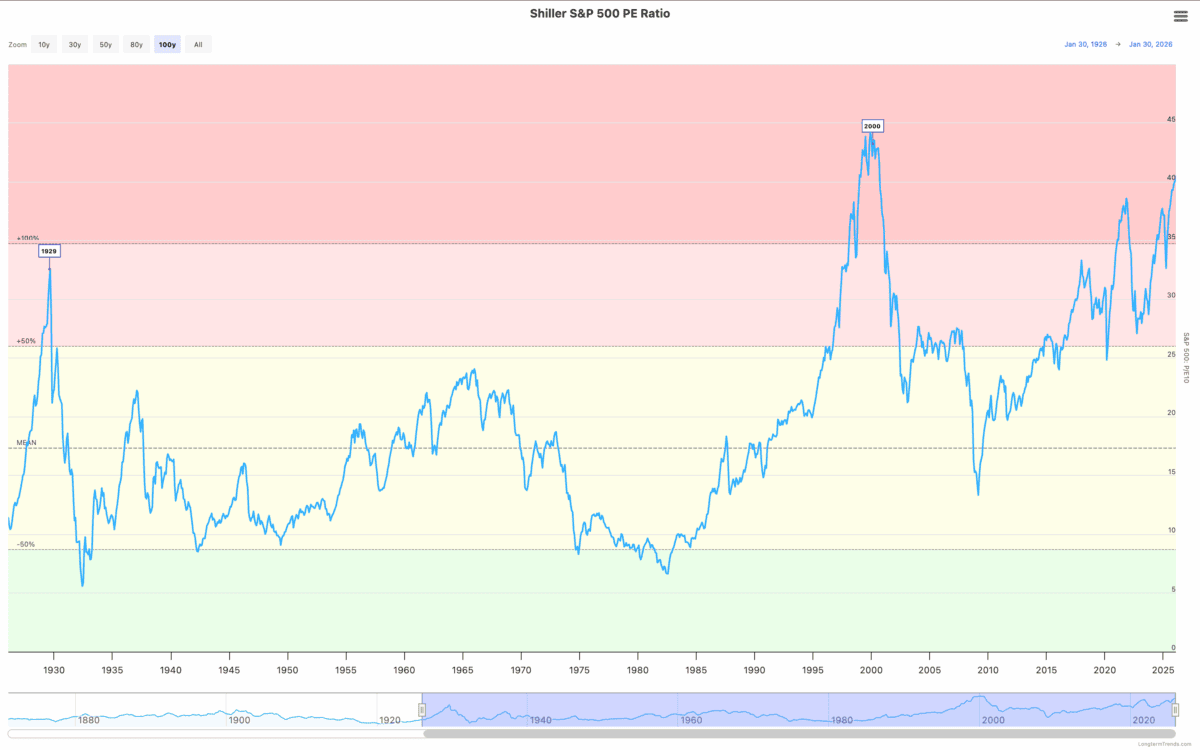

Adjusting for cyclicality, the one time the S&P 500 has been costlier than it’s proper now was in 2000. Proper earlier than the dotcom crash noticed tech shares plunge.

Buyers can’t ignore this, however the concern is what they need to do about it. And the reply isn’t essentially to start out promoting shares – and even to cease shopping for.

Inventory market crash

It’s nearly unattainable to disregard the similarities between the inventory market in 2000 and immediately. The rise of synthetic intelligence seems to be lots just like the emergence of the web.

The casualties from the dotcom crash have been enormous. Some shares fell greater than 90% and traders who purchased them at their peaks are nonetheless ready for them to recuperate.

Exterior of tech, there have been shares that didn’t simply maintain their worth, however really went up as traders appeared for security. These have been shares in sectors similar to client defensives and utilities.

One technique for traders in search of US shares within the present market is due to this fact to look exterior of AI for potential stability. However I feel this can be a dangerous strategy that wants dealing with with care.

Going defensive

One of many shares that fared nicely within the 2000 crash was Procter & Gamble (NYSE:PG). There are apparent the explanation why – it has a robust place in a market the place demand is regular.

The inventory might maintain up nicely if the market sells off once more. However it’s underperformed the S&P 500 since 2000 and traders have to resolve whether or not this can be a true long-term alternative.

Income development over the past decade has been under 2% a yr. And the inventory trades at a price-to-earnings (P/E) ratio of twenty-two, which isn’t precisely low-cost.

That’s not a criticism – development alternatives simply haven’t been there lately. However traders want to consider the inventory as a long-term funding not simply short-term hypothesis.

Staying the course

When fascinated with the crash of 2000, it’s simple to neglect that the very best transfer for lots of traders was to remain put. Amazon (NASDAQ:AMZN) is a superb illustration of this.

The corporate’s share value fell over 95% when the dotcom bubble burst. However even traders who purchased on the very prime are up greater than 14,000% on their funding simply by holding on since then.

There’s an excellent purpose for this. Amazon has taken a disciplined strategy to worth creation for shareholders. Its on-line platform has created a dominant place by specializing in the long run.

By aggressively specializing in clients, it’s established a scale that makes it nearly unattainable for different companies to compete with. And the remainder has adopted from there over time.

What I’m doing

I maintain Amazon inventory and the corporate is true within the thick of the AI spending. And there’s an actual threat that this won’t repay if demand doesn’t materialise as anticipated.

In that state of affairs, the share value would possibly go down. However I’m a purchaser, relatively than a vendor, at immediately’s ranges – even with the S&P 500 at traditionally excessive valuation ranges.

To my thoughts, the lesson of historical past is fairly clear. Buyers who can determine companies with long-term aggressive benefits don’t want to fret about short-term inventory market crashes.

Plummets 8% As Bitcoin Hits One‑Year Lows")

{kind=link}